Top Credit Card Issuers in the US

- Chase

Chase offers a wide portfolio of credit cards, particularly strong in travel and dining rewards. Its products are best suited for consumers with good to excellent FICO scores. - American Express

American Express emphasizes premium experiences, including lounge access, concierge services, and superior dispute resolution, appealing to frequent travelers and business users. - Capital One

Capital One combines flexible approval standards with competitive cash back and travel rewards, making it attractive to both new and experienced cardholders. - Discover

Discover targets US-based consumers seeking simplicity, offering rotating cash back, no annual fees, and easy-to-understand terms. - Navy Federal Credit Union

Navy Federal focuses on long-term financial stability for its members, offering lower interest rates and strong customer support rather than aggressive rewards.

Major Bank Credit Cards

Large US banks issue credit cards with attractive sign-up bonuses, long 0% intro APR periods, and flexible rewards programs. These cards are widely accepted and include security features like zero-liability fraud protection. However, carrying balances can become costly due to high APRs, making careful management essential.

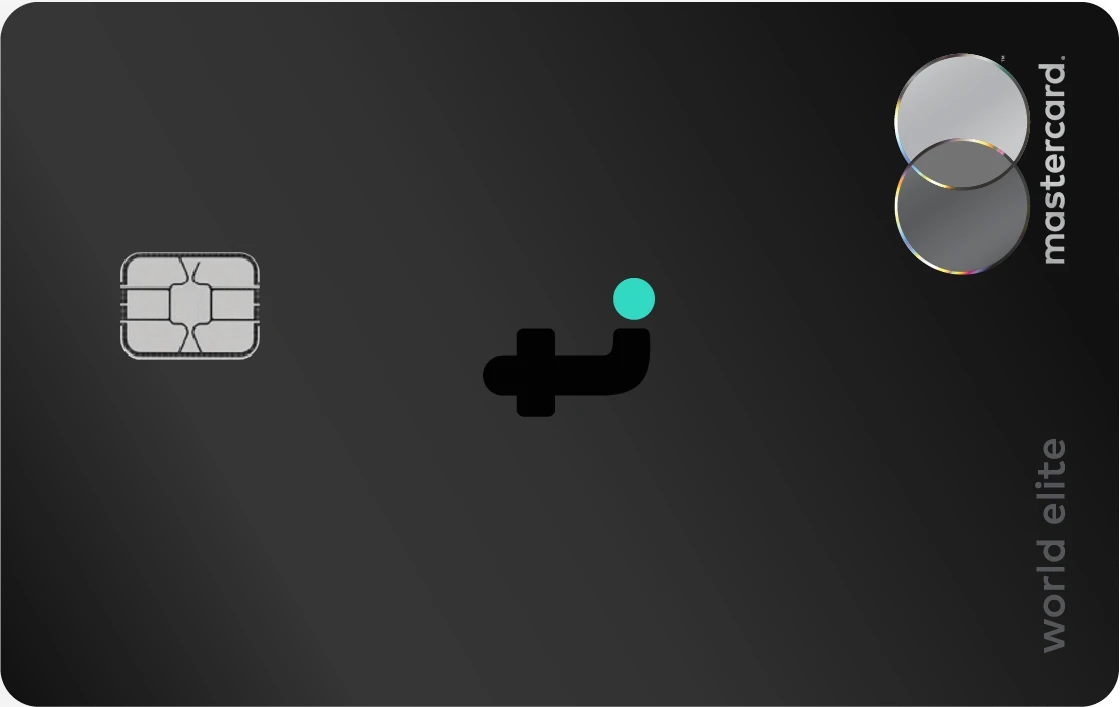

Tomo Credit Card Mastercard

The Tomo Credit Card Mastercard removes traditional credit barriers by eliminating interest and FICO-based approval. Instead of revolving balances, Tomo automatically pays your statement from a linked US bank account. With no annual fee, credit bureau reporting, and broad Mastercard acceptance, Tomo is ideal for consumers focused on long-term credit health rather than short-term rewards.

Fintech or Online-Only Credit Card Issuers

Online-only issuers emphasize speed, transparency, and app-driven controls. Many offer instant approvals and budgeting tools, making them appealing to younger or first-time US cardholders. The trade-off may include fewer premium benefits and limited phone-based customer support.

Secured Credit Cards for Building Credit

Secured cards require a refundable deposit and are widely used to establish credit history. They report payment behavior to credit bureaus, helping users build their FICO score, though they usually offer minimal perks.

Retail Store Credit Cards

Retail credit cards often entice shoppers with exclusive discounts, but they typically carry high interest rates and limited spending flexibility. These cards should be used carefully and paid off immediately.

How Credit Cards Impact Your Finances and Credit Score in the US

Your credit card habits directly affect your FICO score, particularly payment history and credit utilization. Low balances and timely payments improve your score, while high-interest debt can grow quickly. Credit card balances also factor into your debt-to-income ratio, influencing mortgage and loan approvals.

Balance transfers can help consolidate debt but require careful planning. Card perks like purchase protection and rental car coverage can save money when understood. Applying for multiple cards quickly can trigger several hard inquiries, temporarily lowering your score. Reading the cardholder agreement and paying balances in full remains the best strategy.