Top Credit Card Issuers in the US

- Chase – One of the most influential card issuers in the US, offering a wide range of cash back and travel-focused cards with strong digital tools.

- American Express – Best known for premium rewards, exceptional customer service, and cards tailored to frequent travelers and diners in the US.

- Capital One – Appeals to a broad audience with simple cash back structures, accessible approvals, and intuitive mobile banking features.

- Discover – Offers consumer-friendly credit cards with no annual fees, rotating cash back categories, and US-based customer support.

- PenFed Credit Union – A respected credit union providing competitive APRs and solid rewards for qualifying US members.

1. Major Bank Credit Cards

Major bank credit cards in the US are widely accepted and often include features like cash back rewards, travel points, and 0% intro APR offers on purchases or balance transfers. These cards typically provide strong fraud protection and account management tools. However, they usually require good to excellent credit and may charge higher APRs once introductory offers expire.

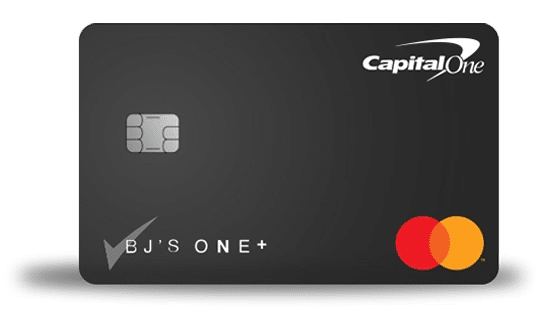

2. BJ’s One Mastercard

The BJ’s One Mastercard is tailored for US consumers who frequently shop at BJ’s Wholesale Club. It offers cash back on BJ’s purchases, gas, and grocery spending, aligning well with common American household expenses. The card has no annual fee, a straightforward rewards structure, and a simple online application process. Backed by a major US issuer, it delivers reliable customer service, standard Mastercard protections, and broad acceptance throughout the United States.

3. Fintech or Online-Only Credit Card Issuers

Fintech and online-only credit card issuers emphasize speed, transparency, and mobile-first design. Many offer instant approvals, real-time notifications, and flat-rate cash back. These cards are attractive to tech-savvy Americans but may lack traditional perks like travel insurance or extended customer support options.

4. Secured Credit Cards for Building Credit

Secured credit cards are commonly used in the US to establish or rebuild credit. They require a refundable security deposit that sets the credit limit and report payment activity to major credit bureaus. While rewards are limited, responsible use—such as low balances and on-time payments—can steadily improve a FICO score.

5. Retail Store Credit Cards

Retail store credit cards often promote exclusive discounts or special financing offers, but they typically come with high APRs and limited usability. For US consumers, these cards can help build credit if managed carefully, but carrying a balance can quickly lead to costly interest charges.

How Credit Cards Impact Your Finances and Credit Score in the US

Credit cards play a major role in determining your FICO score, with the credit utilization ratio being one of the most important factors. Keeping balances below 30% of your available credit is critical. On-time payments build a strong credit history, while high balances accrue expensive compound interest. Credit card debt also affects your debt-to-income (DTI) ratio, influencing approval odds for major loans like mortgages. Balance transfers can help manage debt when used responsibly. Benefits such as purchase protection and rental car insurance add value, but multiple hard inquiries in a short period can lower your score. Always read the cardholder agreement, avoid high-interest debt, and aim to pay your balance in full whenever possible.